Insight, inspiration and education

Understanding how the financial system and banking industry works can help us to get the most out of our savings and investments. Here our founders and partners share some of their knowledge.

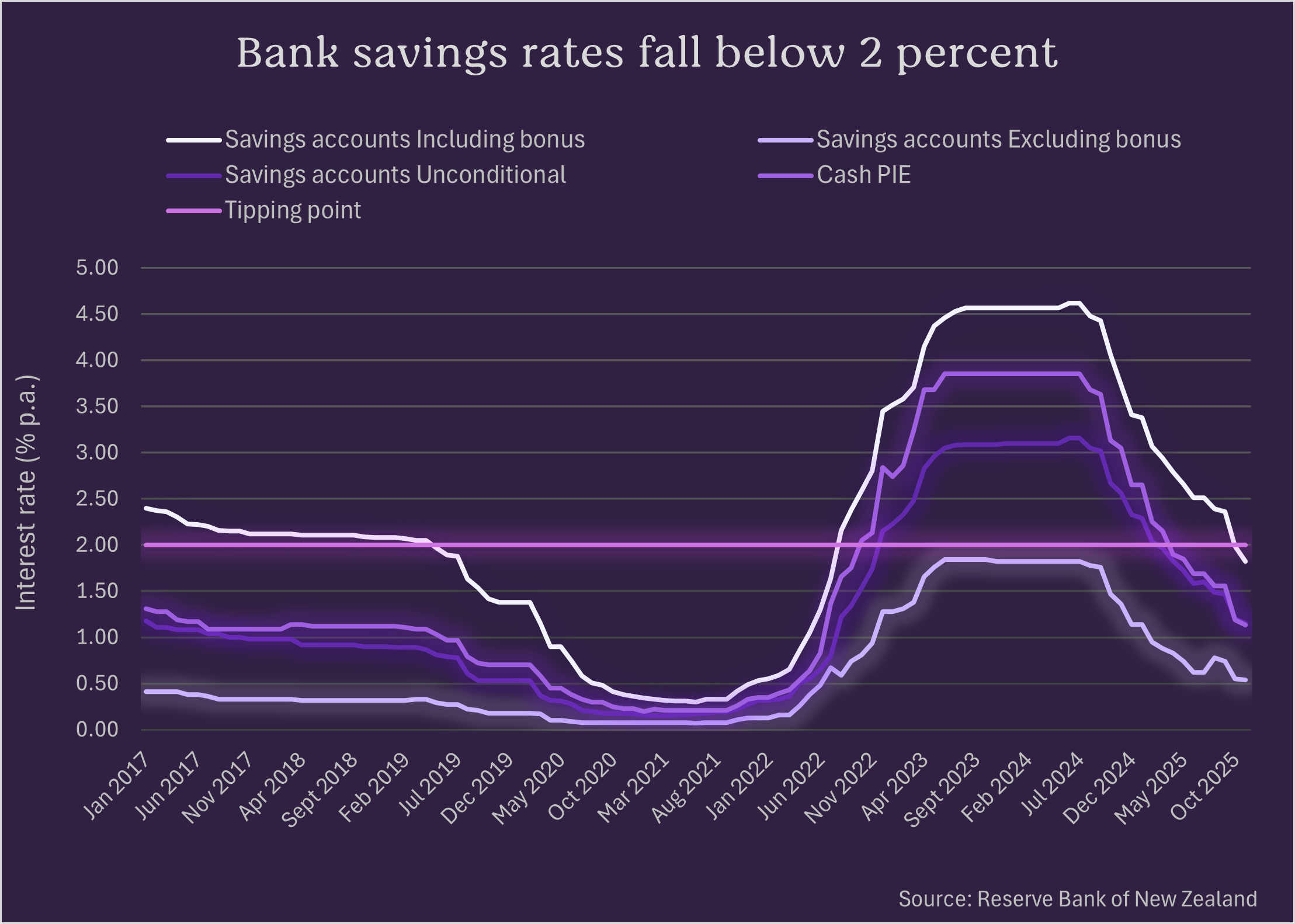

Yield vs. Rate explained

Quick Rule of Thumb

When you see the word “yield,” you’re looking at an investment product. When you see “savings rate” or “interest rate,” you’re looking at a savings product. Understanding this very big difference is the secret to avoiding a surprise down the track.

Yield: As good as a guess

You can think of a yield like a long-range weather forecast. It tells you what the conditions could be for the next year – based on everything staying exactly the same. Which means it's the return you could earn on your investment (but probably won’t) over the next year.

It makes big assumptions - including the current portfolio not changing and markets not moving.

Fees often sit behind the number - as the fund manager’s fees are often deducted after the published yield.

It changes constantly - because you are invested directly in the market. This means you get the wins when things go well, but you also carry the losses when they don’t.

Rate: What you see is what you get

A savings or interest rate is more like a "set menu". It’s designed to give you one thing: reliability.

It's a commitment. A rate isn't a "maybe". It’s the actual pace at which your balance grows each day.

It's all-inclusive. Rates are almost always quoted after fees. The number you see is the number that hits your account before tax.

It removes surprises. The complexity of the market remains behind the scenes. You aren't directly exposed to short-term market variability. That’s for the provider to manage, not you.

Why this matters for your wallet

Confusion happens when people treat yields and rates as interchangeable. They are not at all comparable.

An investment product offers the "upside" of beating a forecast, but it also comes with the "downside" of missing it. While a savings product trades this for reliability.

Where a Savings Fund fits in

The Wedge Savings Fund was built specifically for people who value clarity. While we work hard behind the scenes managing a high-quality portfolio of cash-equivalent assets on your behalf, we don't want you to have to do the guessing.

That’s why the Fund offers a Set Rate of return. We take care of the market's ups and downs for you; in exchange for that consistency, any extra performance the portfolio earns stays with Wedge.

The Bottom Line

Investment funds are about performance. Savings funds are about peace of mind.

.png)